When it comes to managing your finances, understanding the distinction between saving and investing is crucial. Both strategies play significant roles in achieving different financial goals. While saving is typically associated with short-term needs, investing is more about long-term wealth accumulation.

This article explores the nuances of the topic Saving vs. Investing: What’s Best for Your Financial Goals? and provides insights into how you can effectively manage your money depending on your personal objectives.

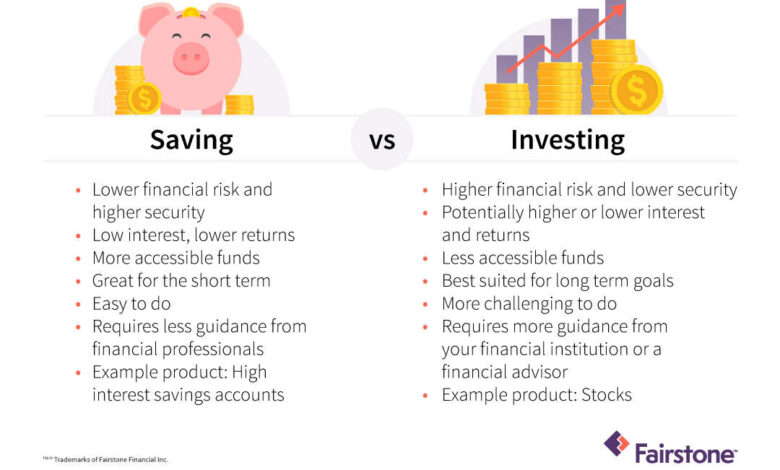

How do saving and investing differ?

Saving and investing serve different purposes, and it’s essential to understand these differences. Saving generally refers to setting aside money for short-term goals or emergencies. This money is typically kept in a savings account or similar low-risk vehicle where it can be quickly accessed. In contrast, investing involves using your money to purchase assets like stocks and bonds with the expectation that their value will increase over time, thus yielding higher returns.

One of the key differences is risk. Savings are often insured and provide a safe harbor for your funds, whereas investments come with varying levels of risk that can lead to gains or losses.

Time horizon also plays a significant role. Savings are best for immediate needs, while investing is suitable for long-term goals. Understanding these differences can help you align your financial strategy with your personal objectives.

What are the benefits of saving?

There are numerous advantages to having a robust savings plan. First and foremost, savings offer liquidity, allowing you to access your funds quickly when needed. This is particularly beneficial for emergencies, such as unexpected medical expenses or car repairs.

Additionally, saving can help build financial stability. Maintaining a solid savings account can provide peace of mind and a safety net for life’s uncertainties. Furthermore, the interest earned on savings accounts, though often modest, can still contribute to your overall financial health.

- Provides immediate access to funds.

- Helps cover unexpected expenses or emergencies.

- Builds financial security and peace of mind.

- Can earn interest, albeit usually lower than investments.

In summary, a strong emphasis on saving can be particularly beneficial for short-term financial goals and emergencies, ensuring that you have the necessary funds when you need them most.

What are the benefits of investing?

Investing offers the potential for higher returns compared to saving, making it an essential component of long-term financial planning. One significant advantage is the ability to grow wealth over time through compounded returns. For example, investing in a diversified portfolio of stocks, bonds, or mutual funds can lead to substantial growth over several years.

Moreover, investments can keep pace with or outstrip inflation, helping to maintain your purchasing power. This characteristic is particularly important in today’s economic climate, where inflation can erode the value of saved money.

- Potential for significant long-term growth.

- Ability to outpace inflation and maintain purchasing power.

- Offers diversification, reducing overall risk.

- Can generate passive income through dividends and interest.

Incorporating investments into your financial strategy can be enormously beneficial for achieving goals like retirement, education, or major purchases.

How much should I save vs. invest?

Determining the right balance between saving and investing largely depends on your financial situation and objectives. A common strategy suggests setting aside enough in savings to cover three to six months’ worth of expenses, creating a solid emergency fund first.

Once you have a robust savings buffer, you can begin to allocate funds towards investments. A good rule of thumb is to prioritize investing for long-term goals, while continuing to contribute to your savings for short-term needs.

Another aspect to consider is your risk tolerance. If you are more risk-averse, you might choose to save a larger percentage of your income. However, if you are comfortable with risk, you may lean towards investing more.

When is the right time to start investing?

The right time to start investing can vary significantly based on individual circumstances. However, many financial experts recommend starting as early as possible, especially when considering the compounding effect of returns. Even small amounts can grow substantially over time.

It’s important to ensure that you are financially stable before investing. This includes having an emergency fund in place and being free from high-interest debt. Once those conditions are met, you can begin to explore various investment options to help achieve your long-term goals.

Additionally, consider your life stage. Younger investors may have a longer time horizon and can afford to take on more risk, while those closer to retirement might prioritize preserving capital.

What are the risks of saving and investing?

While saving is generally considered low-risk, there are still potential downsides. For example, the interest earned on savings often does not keep pace with inflation, meaning that money saved today could lose value over time.

Investing, on the other hand, comes with various risks, including market volatility and the potential loss of principal. The value of investments can fluctuate based on economic conditions and market performance, which can be unsettling for some investors.

It’s crucial to assess your risk tolerance and align it with your financial goals. A diversified investment portfolio can help manage risk by spreading it across different assets.

How can a financial advisor help with saving and investing?

A financial advisor can be invaluable in guiding your saving and investing strategies. They can help you create a personalized financial plan that reflects your unique goals, risk tolerance, and time horizon. Advisors can also assist in selecting the right investment vehicles, such as 401(k) plans or IRAs, that align with your objectives.

Moreover, an advisor can provide ongoing support and adjustments to your financial plan as your circumstances change. Whether you’re saving for a new home or planning for retirement, their expertise can help ensure that you’re on the right track.

Finally, a financial advisor can help you understand the complexities of investing, making it easier to navigate the financial landscape and make informed decisions.

Questions related to saving and investing

Is it better to save or invest your money?

The answer depends on individual financial goals. If you’re focusing on short-term goals, saving may be more beneficial due to its liquidity and safety. However, for long-term objectives where wealth accumulation is key, investing is generally the better option.

What if I invested $1000 in S&P 500 10 years ago?

If you had invested $1000 in the S&P 500 ten years ago, you would have likely seen substantial growth. Historically, the S&P 500 has provided an average annual return of around 10%. This means that your investment could have grown significantly, demonstrating the power of long-term investing.

What is the 7% rule in investing?

The 7% rule suggests that, historically, a diversified investment portfolio can expect to earn an average annual return of approximately 7% after adjusting for inflation. This rule serves as a guideline for long-term investors aiming to project future growth based on past performance.

What is the 10/5/3 rule of investment?

The 10/5/3 rule is a strategy for asset allocation based on your age. For example, if you are 30 years old, you may invest 10% in stocks, 5% in bonds, and 3% in cash equivalents. This rule helps ensure a balanced approach to investing that aligns with your risk tolerance and time horizon.