In today’s unpredictable economic climate, families face numerous financial challenges. Making sound financial decisions is essential for stability and growth. This article explores crucial strategies and tips to help families navigate these uncertain times effectively.

How can families prepare financially for economic uncertainty?

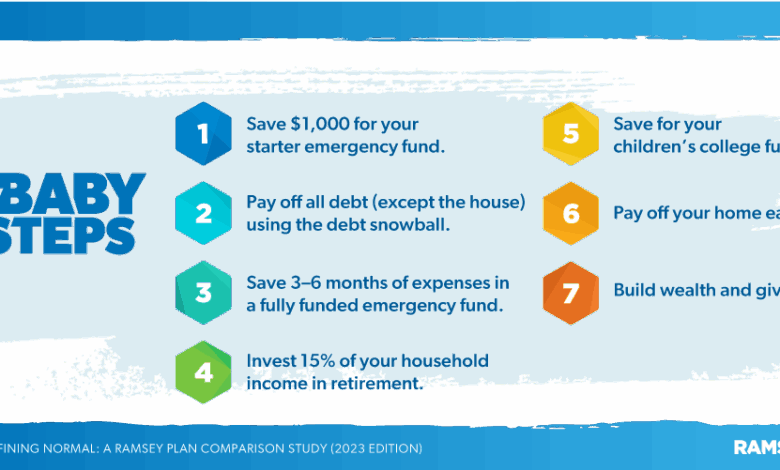

Preparing for economic uncertainty requires a proactive approach to financial planning. Building a solid emergency fund is one of the first steps families should consider. Ideally, this fund should cover three to six months of living expenses, providing a financial cushion during tough times.

Understanding potential sources of income loss is also vital. Families need to evaluate their job security and explore alternative income streams, such as freelance work or side businesses. This diversification can help mitigate risks associated with sudden job loss.

Additionally, families should regularly review their expenses and identify areas where they can cut back. This can free up funds to bolster savings and reduce financial stress. Implementing a zero-based budgeting method may help in aligning priorities with spending.

What are the key components of a solid financial plan?

A robust financial plan is crucial for families aiming to secure their financial future. Key components include:

- Budgeting: Creating a detailed budget that tracks income and expenses helps families maintain financial discipline.

- Emergency savings: As mentioned earlier, having an emergency fund is essential for unexpected circumstances.

- Debt management: Families should prioritize paying off high-interest debts to avoid financial strain.

- Investment strategy: Developing a diversified investment portfolio can enhance wealth over time.

Moreover, families should engage in regular risk assessments to evaluate their financial health. This includes monitoring expenses, income sources, and potential market fluctuations.

Consulting with financial advisors can provide personalized insight tailored to a family’s unique situation. These professionals can guide families through complex decisions, ensuring their financial plans are sound.

How often should families update their financial plans?

Regular updates to financial plans are essential as circumstances change. Families should review their plans at least once a year or during significant life events, such as:

- Changes in income, such as job loss or promotions.

- Major life events like marriage, divorce, or the birth of a child.

- Shifts in financial goals, such as saving for college or retirement.

Updating financial plans helps families adapt to new challenges and opportunities. It is crucial to assess the effectiveness of current strategies and make necessary adjustments to remain on track.

Families should also stay informed about economic trends that might impact their financial situation. This proactive approach enables them to respond to changes in the economy swiftly.

What budgeting strategies are effective during tough economic times?

During challenging economic periods, families must adopt effective budgeting strategies. One approach is the 50/30/20 rule, which allocates 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. This method simplifies budgeting and promotes savings.

Another effective technique is zero-based budgeting, where every dollar is assigned a job, whether saving, spending, or investing. This can lead to more mindful spending and better financial control.

Families can also benefit from using budgeting apps to track expenses and visualize their financial health. These tools provide insights into spending habits, helping families make informed decisions about where to cut back.

How can families manage debt in an uncertain economy?

Managing debt during uncertain times is vital for financial stability. Families should prioritize paying down high-interest debts first, as these can accumulate quickly and lead to financial distress.

Utilizing debt management tips for uncertain times, such as consolidating loans or negotiating lower interest rates, can be beneficial. This can reduce monthly payments and make debt more manageable.

Families should also consider creating a debt repayment plan. This could involve the snowball method, where smaller debts are paid off first to build momentum. Alternatively, the avalanche method focuses on paying off debts with the highest interest rates first, which can save money in the long term.

Ultimately, maintaining open communication about finances within the family is crucial. Discussing financial challenges and strategies can foster collaboration and support in overcoming debt.

What investment strategies should families consider?

When it comes to investing during uncertain economic times, families should focus on investment strategies for families in a recession. Diversification is key; spreading investments across various asset classes can mitigate risks associated with market fluctuations.

Families should also assess their risk tolerance before making investment decisions. Those more comfortable with risk might explore strategies such as short selling or tax-loss harvesting, which can enhance returns in volatile markets.

Long-term investments in fixed-income assets can provide stability during downturns. However, families must remain mindful of potential risks associated with these types of investments, including interest rate changes.

Lastly, consulting with qualified financial professionals can provide invaluable guidance. These experts can help families navigate complex investment landscapes and develop strategies aligned with their financial goals.

Exploring Related Questions About Financial Planning for Families

How to manage finances during economic uncertainty?

Managing finances effectively during economic uncertainty requires a multifaceted approach. Families should focus on creating a detailed budget, identifying essential expenses, and cutting non-essential costs. Developing an emergency fund can provide additional security for unexpected situations. Furthermore, regular financial reviews can help families adapt their strategies as conditions change.

Education on financial literacy is also vital. Families can benefit from resources such as workshops, webinars, and books focused on personal finance. This knowledge empowers them to make informed decisions, enhancing their financial resilience.

What is the 50/30/20 rule in financial planning?

The 50/30/20 rule is a simple budgeting guideline that divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. This approach helps families prioritize essential expenses while ensuring they allocate funds toward savings and debt reduction.

By adhering to this rule, families can gain better control over their finances. It encourages mindful spending habits and promotes a clear understanding of where money is allocated, leading to improved financial health.

What is the 7% rule in finance?

The 7% rule in finance suggests that investors can expect an average annual return of around 7% on their investments over the long term, accounting for inflation. This rule serves as a guideline for families planning for retirement or other long-term financial goals.

Understanding this rule can help families set realistic expectations for their investment growth. It encourages a focus on long-term strategies rather than short-term fluctuations, fostering a disciplined approach to investing.

What is the 1234 financial rule?

The 1234 financial rule is a budgeting strategy that emphasizes simplicity. It suggests allocating 1% of income to savings, 2% to debt repayment, 3% to necessary expenses, and 4% to discretionary spending. This method helps families maintain balance in their finances while ensuring they prioritize saving and debt reduction.

Adopting this rule can assist families in establishing a healthy financial foundation. It encourages responsible spending and emphasizes the importance of savings in achieving financial goals.

In summary, effective financial planning is paramount for families navigating an uncertain economy. By implementing these strategies, families can enhance their financial resilience and secure their economic future.